(国际投行研究报告 凌通社 )

We continue to believe that financial cleanup will support gradual NIM expansion and reduce long-term risks for banks. However, rising trade tensions have increased market risks and could limit near-term upside. We are cutting our H-share/Ashareprice targets by 12%/19% on average.

我们仍然认为金融出清将会得到支持逐步扩大净息差并降低银行的长期风险。然而,不断上升的贸易紧张局势增加了市场风险可能限制近期上涨空间。 我们正在削减我们的H股/ Ashare价格目标平均上涨12%/ 19%。

Potential policy fine-tuning should not change the direction of financial cleanup efforts, and we continue to see upside for China banks on higher NIM, healthy ROE, solid dividend yield and lower long-term risks.

潜在的政策微调不应改变金融出清的方向努力,而且我们继续看好中国银行在净息差上涨方面的健康发展ROE,稳定的股息收益率和较低的长期风险。

Despite some potential policy fine-tuning such as targeted RRR (reserve requirement ratio) cuts and higher local bond issuance, we believe ongoing financial cleanup efforts and related policies will lead to some further moderation in total credit growth and hence modestly higher average rates in China. Modestly higher asset yields, a better than expected deposit segmentation strategy widely adopted by banks, and potential RRR cuts should help contain the pace of the funding cost increase and support gradual net interest margin (NIM) expansion at banks with strong funding franchises. We do not see a major rebound in NPL formation despite rising bond defaults, considering healthy profit growth and EBIT interest cover at major industrial firms. While each bond default could be sizeable, we believe the cumulative NPLs (nonperforming loans) from bond defaults will not offset the likely lower NPL formation from the industrial sector. We expect rational industrial capacity expansion to reduce the negative impact on corporate profitability and credit quality risks from moderation in macroeconomic growth.

However, rising trade tensions with the US have increased market risks and could delay part of bank re-rating.

然而,与美国的贸易紧张关系不断上升增加了市场风险可能会延迟部分银行重新评级。

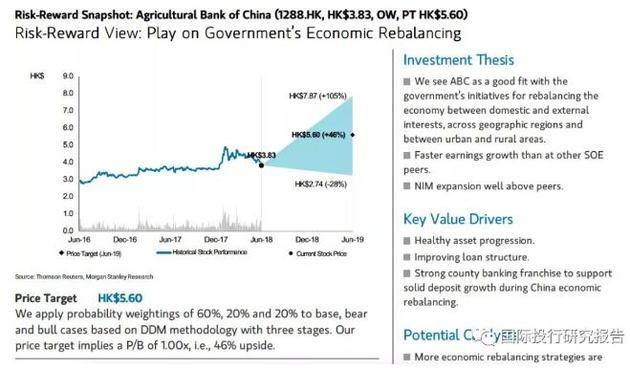

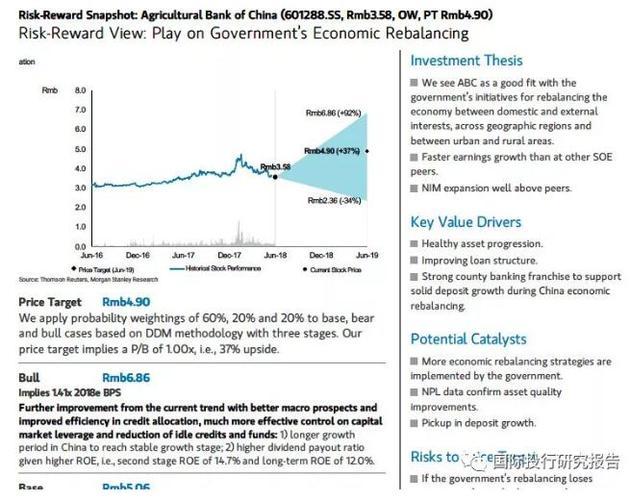

The June 15 and 18 announcements by the US and China of import tariffs indicate escalation of trade tensions that could complicate the macroeconomic outlook. We believe investors may require more evidence of a smooth cleanup process in the banking industry. In light of the higher risks, we raise beta estimates across the board by 0.1x to 1.05-1.5x for banks under our coverage and cut our H-share and A-share price targets by 12% and 19%, respectively, on average, anticipating higher market volatility. Our other changes include: 1) updating 2018 earnings forecasts; 2) raising beta estimates for city commercial banks to reflect potentially higher credit costs and deposit rate volatility due to higher customer concentration; 3) adjusting ROE and beta for selected shareholding banks in light of recent financial results. Our top picks are PSBC, CCB, ABC and CRCB, while we continue to see turnaround opportunities at CITIC Bank and Minsheng.

金融出清应该支持逐步的NIM扩张和减少银行的长期风险